The global information technology industry reached $5 trillion in 2019. As the industry keeps growing, it will also continue diversifying, with emerging technologies like blockchain, cloud, virtual reality and more. Despite a wide range of specialties, all tech companies have one thing in common: they need technology errors & omissions insurance.

Errors & omissions (E&O) insurance is a form of professional liability insurance. It protects your company when mistakes and oversights occur. As you might suspect, the chance of mistakes and oversights increases during times of fast growth and intense innovation. In other words, as a tech company, you’re at high risk of E&O right now.

Types of Tech E&O Lawsuits

Tech companies face a range of liability risks. For example, technology product glitches and service interruptions can lead to major downtime, and your clients can lose business and reputation as a result. If a client suffers a financial loss because of your product or service, your E&O policy would protect your business by providing legal defense and insurance coverage.

Other E&O risks come from data and sharing complexities. As technology enables us to collect and store more data, data management and protection has gotten complicated. New laws, including the GDPR and the California Consumer Privacy Act, restrict how data can be used and shared. Tech companies that don’t comply can face significant penalties.

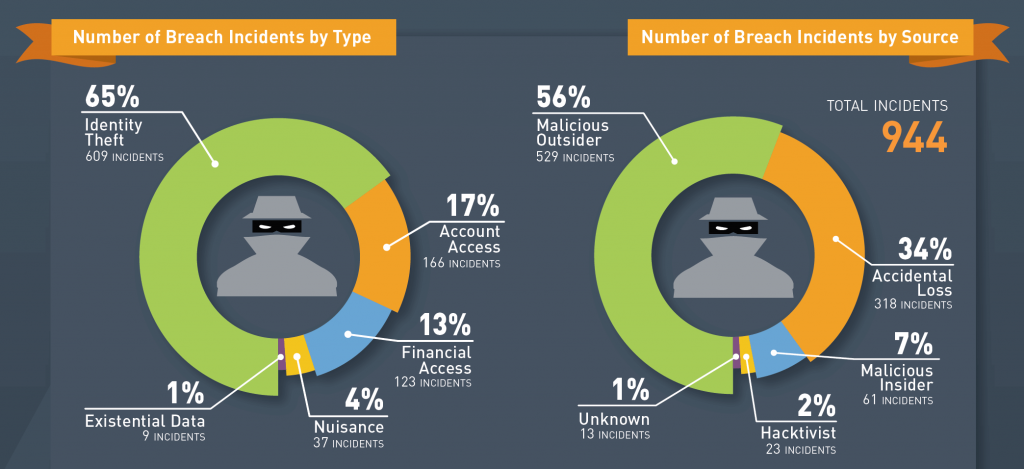

Tech companies also face the risk of security breaches and cyber-attacks. According to the Breach Level Index, more than 6 million records are lost or stolen every day. Tech companies handle sensitive data, and they have a responsibility to keep it safe. Unfortunately, hackers are constantly launching new attacks, while simple human error can also result in security problems.

When something goes wrong, expensive lawsuits can follow. Some of the possible E&O claims you could encounter include:

1. Failure to perform or breach of contract

If your company promises a service or product and doesn’t deliver, a lawsuit may be the result. This could be caused by unexpected technical difficulties or other issues.

2. Negligence

Mistakes and carelessness happen. An employee might forward an email containing sensitive information to the wrong person, for example, or leave a laptop in the wrong place. When it results in financial loss or data breaches, human error can become the basis of legal action.

3. Theft of Personally Identifiable Information (PII) and failure to prevent the introduction of malicious code

If a cybercriminal succeeds in infecting your software with a virus and uses it to steal names, addresses, Social Security Numbers and other types of PII, you can be held responsible for failing to prevent it.

4. Copyright infringement

Copyright protection extends to code and software. If your tech company is accused of using copyright protected software, you could be facing an expensive court battle. It can happen in the reverse, too. Another company could steal your software. To protect your rights, you’ll need to file a lawsuit, and that can be a time-consuming and costly process.

5. Defamation in online content

Many companies allow user-generated content, such as reviews and comments. If any of this content is libelous in nature, your tech company could be held responsible. Likewise, if the defamatory online content of another company causes damage to your company, you may need to file a lawsuit to recoup your losses.

How E&O Cases Can Play Out

To see how E&O claims can play out in the tech sphere, let’s look at an example. A medical billing company needed to integrate the records of a large pharmaceutical distributor across several networks. It hired a software company specializing in software to integrate data across multiple platforms.

When the pharmaceutical company needed their data, it was discovered that the software had failed and had destroyed over 30% of the records. This resulted in fines and lost revenue of over $2,840,000. The pharmaceutical company sued the medical billing company and the software manufacturer and was awarded $3,000,000 plus punitive damages at trial.

Another, more famous, example can be seen in the case of Oracle v. Google. Back in 2010, Oracle sued Google over claims that Google has been running a program that infringes on Java’s patent. Google has claimed that the use of the APIs in question falls under fair use.

In 2018, the United States Court of Appeals for the Federal Circuit ruled in favor of Oracle. Oracle is seeking more than $8 billion in damages, while Google is appealing to the Supreme Court of the United States. For both parties, the nine-year court sage has consumed considerable resources.

How Tech E&O and Cyber Liability Insurance Policies Work Together

You may be wondering about the differences between Tech E&O and cyber liability insurance policies. The first thing to know is that you should have both types of coverage.

- Tech E&O insurance provides tech companies with coverage for errors, omissions, negligence and product failures that may occur.

- Cyber liability insurance can provide first-party and third-party coverage for financial loss resulting from data breaches and other cyber events.

Both policies are important, but there can be some coverage overlap. This is why it’s beneficial to combine policies in a bundle with one carrier. Doing so provides clear coverage boundaries, avoids gaps in coverage and may help you control costs.

This is especially true considering how common and diverse cyber risks are. If a loss occurs, there could be a question as to whether the loss falls under the realm of Tech E&O or Cyber Liability coverage. If both coverages are with one insurer, there’s less risk that a claim could be denied.

How to Get the Most out of Your E&O Policy

Most importantly, don’t underestimate your need for insurance. Technology is the most sued sector according to the Securities Class Action Clearinghouse. Assume that you will be sued at some point and prepare accordingly.

How much you pay for tech E&O coverage will depend on several factors.

- How big is your company?

- What products and services do you provide?

- Is the technology provided emerging and new or established and proven?

- How large are your contracts?

- What are your company’s specific risks and how are they managed?

- What coverage limits do you need?

- How experienced is your team?

- What is your company’s litigation history?

Cost isn’t the only element that’s important when you’re looking at your E&O policy. You also should consider the insurer’s financial strength (A.M. Best Rating) as well as the carrier’s experience in your industry.

Conclusion

Tech companies should also look at policies designed specifically for tech risk. The tech industry is constantly developing new advancements. Tech-tailored E&O policies are designed to keep pace with your industry’s innovations.

Finally, it’s important to understand what is and is not covered. Some claims are typically excluded from tech E&O policies because they are covered by other types of insurance. For example, bodily injury and property damage are covered by other types of insurance policies, such as general liability and property.

Additionally, certain types of claims, such as those caused by delays or breach of contract, may be excluded from some policies. It can take time to find a policy that includes the needed coverages for your business. Know and understand the risks so you can make sure you have adequate protection that works for you.